628 Pips, XAUUSD 16 Points, US500 56 Points and BTC 177 Points Potential Trading Performance from 14 Events in Q1 2026 with Haawks G4A Machine-Readable Data Feed

According to Haawks G4A analysis, the first quarter of 2026 generated a cumulative 628 pips / ticks of potential trading performance, plus notable moves in XAUUSD, US500 and BTC, across major U.S. macroeconomic and commodity data releases.

From USDA crop reports and DOE energy inventories to CPI and Employment Situation releases, Q1 2026 once again showed how scheduled economic data can trigger sharp, short-lived market reactions across futures, FX, equities, gold and crypto.

The key takeaway was clear: news-driven volatility remains fast, measurable and highly time-sensitive.

Q1 2026 Performance Snapshot

Across January, February and March 2026, Haawks G4A tracked potential trading opportunities from the following events:

January 2026: 391 pips / ticks, US500 13 points, BTC 177 points

February 2026: 183 pips / ticks, US500 12 points

March 2026: 54 pips / ticks, XAUUSD 16 points, US500 31 points

Total Q1 2026 indicative performance:

628 pips / ticks, plus XAUUSD 16 points, US500 56 points and BTC 177 points

For comparison, the full-year potential performance in 2025 was 1,828 pips / ticks.

Events Covered in Q1 2026

The following releases generated measurable short-term market reactions:

January 2026

USDA WASDE — World Agricultural Supply and Demand Estimates

200 ticks / 12 January 2026

US BLS Consumer Price Index

5 pips, US500 13 points, BTC 177 points / 13 January 2026

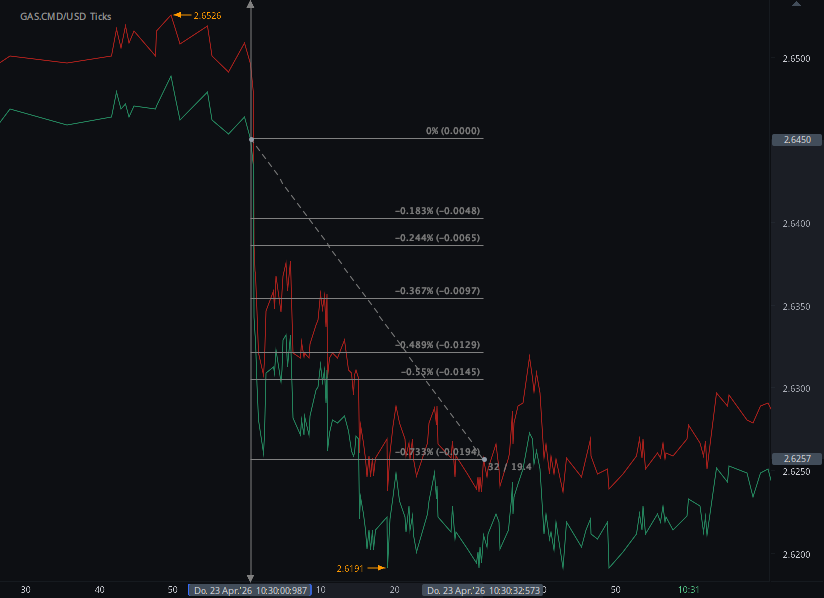

DOE Natural Gas Storage Report

66 ticks / 15 January 2026

DOE Natural Gas Storage Report

103 ticks / 22 January 2026

DOE Natural Gas Storage Report

17 ticks / 29 January 2026

February 2026

US Employment Situation — Non-farm Payrolls

60 pips / 11 February 2026

DOE Natural Gas Storage Report

23 ticks / 12 February 2026

US BLS Consumer Price Index

16 pips, US500 12 points / 13 February 2026

DOE Natural Gas Storage Report

41 ticks / 19 February 2026

DOE Petroleum Status Report

17 ticks / 25 February 2026

DOE Natural Gas Storage Report

26 ticks / 26 February 2026

March 2026

DOE Natural Gas Storage Report

14 ticks / 5 March 2026

US Employment Situation — Non-farm Payrolls

XAUUSD 16 points, US500 31 points / 6 March 2026

USDA Grain Stocks and USDA Prospective Plantings

40 ticks / 31 March 2026

Total trading time across these events would have been only a few minutes, excluding preparation time.

January 2026: USDA, CPI and DOE Reports Drive the Strongest Month

January was the most active month of Q1, producing 391 pips / ticks of potential performance, plus significant moves in US500 and BTC.

The strongest single move came from the USDA WASDE report on 12 January 2026, which generated approximately 200 ticks across grains.

The report confirmed a supply-heavy agricultural backdrop, with record U.S. corn production, higher ending stocks and large global crop supplies. Soybeans, corn and wheat all reacted sharply as traders priced in abundant supply and shifting expectations for demand.

The following day, the US CPI release on 13 January 2026 generated short-term volatility across multiple asset classes:

EURUSD: 5 pips

US500: 13 points

BTC: 177 points

The inflation data showed price pressures remaining steady rather than accelerating. Headline CPI rose 0.3% month-on-month, while annual CPI stood at 2.7%. Core CPI remained at 2.6%, with shelter and services inflation still important for market expectations.

Natural gas was also a major source of volatility in January. Three DOE Natural Gas Storage Reports generated:

66 ticks on 15 January

103 ticks on 22 January

17 ticks on 29 January

The January 22 report was the largest energy-related move of the month, with a 120 Bcf withdrawal triggering a sharp reaction in natural gas futures. Despite strong withdrawals, inventories remained above five-year averages, which helped keep the broader supply picture relatively comfortable.

February 2026: Macro and Energy Volatility Continue

February produced 183 pips / ticks of potential performance, plus US500 12 points, across six key events.

The month began with a major macro catalyst: the US Employment Situation report on 11 February 2026. The release generated a combined 60-pip move across USDJPY and EURUSD within a short reaction window.

The employment data showed:

The report was mixed, with strong gains in healthcare, social assistance and construction, but weakness in federal government and financial activities employment.

Two days later, the US CPI release on 13 February 2026 generated further volatility:

The CPI data showed continued inflation moderation, with monthly CPI at 0.2%, annual CPI at 2.4% and core CPI at 2.5%. Energy prices declined, while shelter and medical care remained firm.

Energy reports were again central to February’s performance. DOE Natural Gas Storage Reports generated:

23 ticks on 12 February

41 ticks on 19 February

26 ticks on 26 February

The February 19 release was the strongest natural gas event of the month, with a 144 Bcf withdrawal and inventories 123 Bcf below the five-year average.

The DOE Petroleum Status Report on 25 February 2026 added another 17 ticks in crude oil futures, driven by a significant inventory build and lower refinery activity.

March 2026: NFP, Gold, Equities and USDA Grains

March produced fewer events, but still delivered meaningful market reactions: 54 pips / ticks, plus XAUUSD 16 points and US500 31 points.

The first major event was the DOE Natural Gas Storage Report on 5 March 2026, which generated 14 ticks. The report showed a 132 Bcf withdrawal, with working gas at 1,886 Bcf. The market reaction reflected a balanced but sensitive supply picture, with storage above last year but slightly below the five-year average.

The biggest cross-asset move of the month came from the US Employment Situation report on 6 March 2026.

The data showed an unexpected decline in payrolls:

Gold and equities reacted sharply:

XAUUSD: 16 points

US500: 31 points

Gold benefited from risk-off sentiment, while equity markets repriced growth expectations within seconds of the release.

The final major event of Q1 was the USDA Grain Stocks and Prospective Plantings report on 31 March 2026, which generated approximately 40 ticks in soybean futures.

The report showed a bearish-leaning supply picture:

Even though the data pointed toward rising supply, the market reaction highlighted how positioning, uncertainty and liquidity gaps can create significant short-term volatility around scheduled agricultural releases.

Key Themes from Q1 2026

1. Energy Data Remained a Reliable Volatility Driver

DOE Natural Gas Storage Reports were among the most consistent sources of short-term futures volatility in Q1.

Across January, February and March, WNGSR releases generated repeated tradable reactions, especially when withdrawals differed from seasonal expectations.

The strongest natural gas move came on 22 January 2026, with a 103-tick reaction.

2. USDA Reports Continued to Move Grain Futures

Agricultural data remained highly relevant for futures traders.

The January WASDE report generated the largest single event move of Q1 at 200 ticks, while the March Grain Stocks and Prospective Plantings release added another 40 ticks.

The main market drivers were:

3. U.S. Macro Releases Moved Multiple Asset Classes

CPI and Employment Situation reports affected FX, equities, gold and crypto.

The January CPI release generated moves across EURUSD, US500 and BTC, while February’s CPI moved both FX and equities. The March Employment Situation report produced notable reactions in gold and US500 after a negative payrolls surprise.

This highlights the cross-market nature of macro news trading.

4. Reaction Windows Were Extremely Short

Many of the moves occurred within seconds or under two minutes of the release.

This reinforces the importance of:

Low-latency data delivery

Machine-readable formats

Predefined event preparation

Automated parsing and execution infrastructure

In modern news trading, speed is often the difference between capturing and missing the move.

Final Thoughts

Q1 2026 showed that scheduled economic and commodity data releases continued to generate fast, measurable trading opportunities across multiple markets.

From USDA reports and natural gas inventories to CPI and NFP, market reactions were often immediate and short-lived. The strongest opportunities came from events where the released data differed meaningfully from expectations or forced traders to quickly reassess supply, demand, inflation or growth assumptions.

The main lesson from the quarter is simple:

Data still moves markets — but the window to act is extremely small.

For professional news traders, machine-readable data is no longer optional. It is a core part of competing in markets where reactions are measured in milliseconds and execution speed matters as much as interpretation.

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.