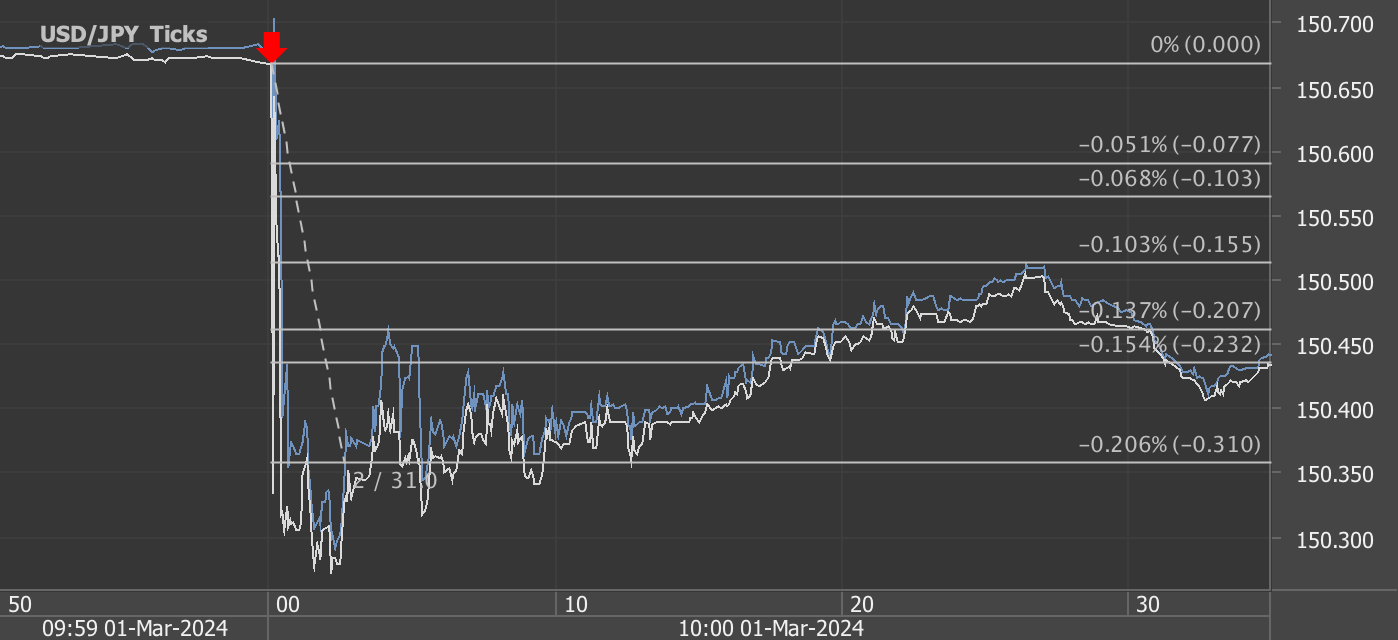

According to our analysis natural gas moved 10 ticks on DOE Natural Gas Storage Report data on 4 April 2024.

Natural gas (10 ticks)

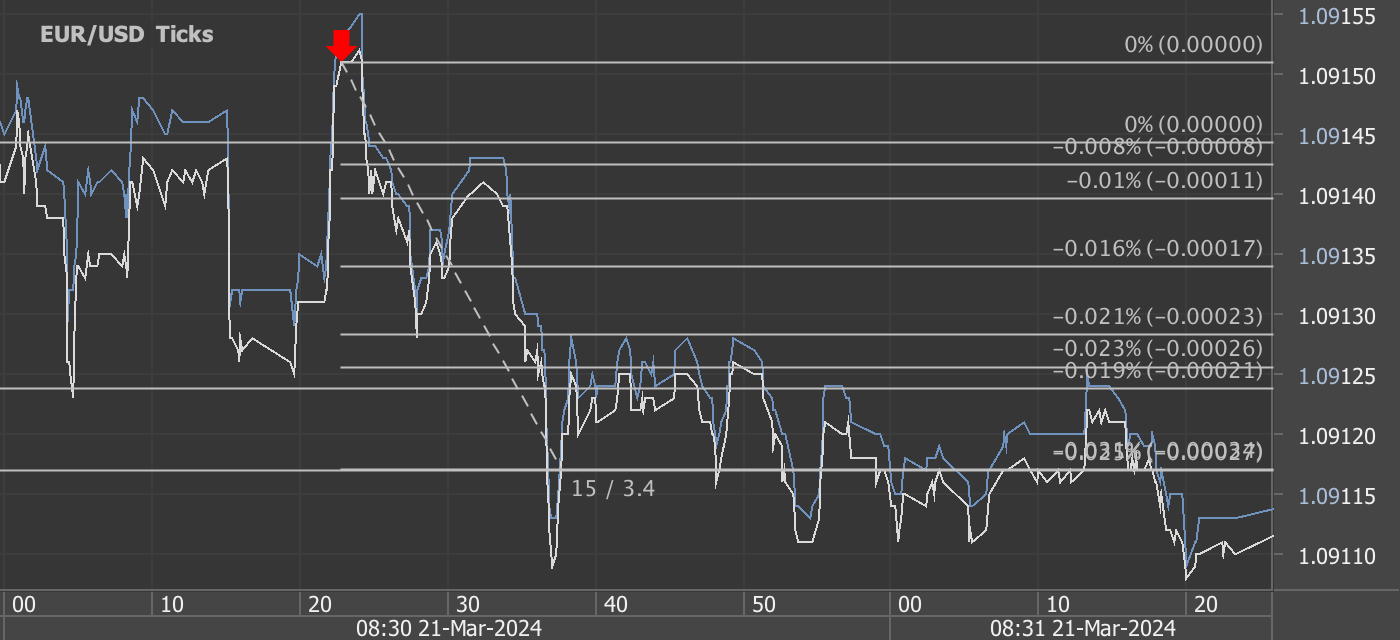

Charts are exported from JForex (Dukascopy).

Analyzing the Latest Shifts in U.S. Natural Gas Storage: A Deep Dive into the Week Ending March 29, 2024

The U.S. Energy Information Administration (EIA) recently unveiled its Weekly Natural Gas Storage Report for the week ending March 29, 2024. This critical snapshot offers invaluable insights into the country's natural gas supply, showcasing a dynamic interplay between demand, storage capacity, and market trends. Here, we delve into the nuances of the latest report, comparing it against historical data to gauge its broader implications on the energy sector and beyond.

Key Highlights from the Latest Report

As of March 29, 2024, working gas in underground storage across the Lower 48 states stood at 2,259 billion cubic feet (Bcf), marking a net decrease of 37 Bcf from the previous week. This shift underscores a significant fluctuation in gas supplies, potentially influencing market dynamics and energy pricing in the short term. Notably, the current storage levels are substantially higher than the previous year's figures and the five-year average, suggesting a robust supply that could stabilize prices and supply chains.

Year-over-Year Increase: Stocks were 422 Bcf higher than the same period last year, presenting a considerable 23% increase.

Five-Year Average Comparison: When measured against the five-year average of 1,626 Bcf, the current storage levels are 633 Bcf above, reflecting a substantial 38.9% increase.

Regional Breakdown: A Closer Look

The report details specific trends across various regions, each with its unique dynamics and implications:

East and Midwest: Both regions saw a net decrease in storage levels, with the East experiencing a 24 Bcf reduction and the Midwest a 18 Bcf drop. Despite these decreases, both areas are still well above their previous year and five-year averages, indicating strong reserves.

Mountain and Pacific: The Mountain region reported a modest 4 Bcf decrease, whereas the Pacific region bucked the trend with a 4 Bcf increase. These changes are particularly striking in the context of their year-over-year and five-year average comparisons, showcasing significant variances in regional supply dynamics.

South Central: This region, which includes both salt and nonsalt storage facilities, reported a net increase of 5 Bcf, further bolstering its already substantial reserves.

Implications and Insights

The current state of natural gas storage in the U.S. paints a picture of strength and resilience. With storage levels comfortably above the previous year and the five-year average, the immediate outlook for natural gas supplies seems secure. This abundance is likely to have several key implications:

Market Stability: Higher storage levels typically translate to more stable natural gas prices, benefiting consumers and industries alike.

Energy Security: Robust storage figures contribute to the nation's energy security, ensuring a steady supply to meet domestic demand.

Policy and Planning: These trends are vital for policymakers and energy companies as they strategize for the future, balancing environmental concerns with energy needs.

Looking Ahead

As the energy landscape continues to evolve, monitoring natural gas storage levels remains critical for understanding broader market trends and preparing for future challenges. The EIA's next release on April 11, 2024, is eagerly awaited for further insights into these trends. With the energy sector at a crossroads, influenced by both geopolitical events and the push towards sustainability, the significance of such data cannot be overstated.

In conclusion, the latest Weekly Natural Gas Storage Report offers a glimpse into the complex dynamics shaping the U.S. energy sector. By providing a detailed analysis of current storage levels and historical comparisons, this report is an indispensable tool for anyone looking to navigate the intricacies of the energy market.

Source: https://ir.eia.gov/ngs/ngs.html

Start futures forex fx commodity news trading with Haawks G4A low latency machine-readable data, one of the fastest data feeds for DOE data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.