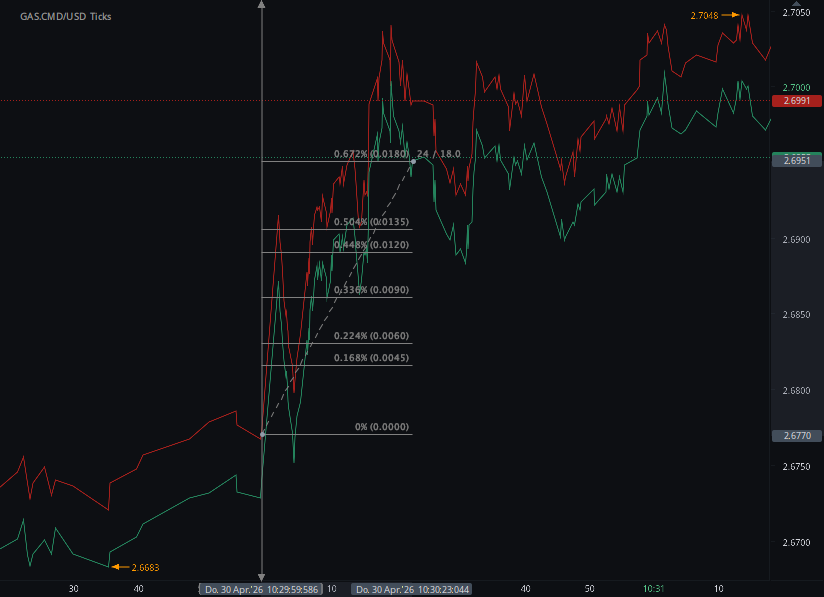

According to our analysis natural gas moved 18 ticks on DOE Natural Gas Storage Report (WNGSR) data on 30 April 2026.

Natural gas (18 ticks)

Charts are exported from JForex (Dukascopy).

Natural Gas Storage Builds Momentum Heading into Late Spring

The latest Weekly Natural Gas Storage Report for the week ending April 24, 2026, offers a clear signal that the injection season is firmly underway. According to the U.S. Energy Information Administration (EIA), working gas in underground storage across the Lower 48 states rose to 2,142 billion cubic feet (Bcf)—a 79 Bcf increase from the prior week.

Strong Weekly Injection Signals Seasonal Shift

This 79 Bcf build is a solid injection for late April, reflecting milder temperatures and reduced heating demand across much of the country. As the market transitions away from winter withdrawals, injections like this are expected to become more consistent in the weeks ahead.

Storage Levels Outpace Historical Benchmarks

Current inventory levels are notably strong:

+116 Bcf higher than the same time last year

+153 Bcf above the five-year average (1,989 Bcf)

Despite these surpluses, total working gas remains within the historical five-year range, suggesting that while supply is comfortable, it is not yet excessive.

Regional Breakdown: Broad-Based Increases

All major regions posted gains during the week:

South Central led with a 26 Bcf injection, bringing total stocks to 905 Bcf

Midwest added 25 Bcf, now at 429 Bcf

East region increased by 23 Bcf, reaching 332 Bcf

Mountain and Pacific regions each posted modest 3 Bcf builds

Within the South Central region:

Salt storage rose by 9 Bcf

Nonsalt storage increased by 18 Bcf

The relatively balanced distribution of injections suggests stable supply conditions nationwide, without any major regional constraints.

Market Implications

The above-average storage levels could exert downward pressure on natural gas prices in the near term, particularly if injections continue at a strong pace and demand remains moderate. However, several factors could shift this outlook:

Early summer heat waves driving cooling demand

LNG export levels

Production trends and rig activity

For now, the market appears well-supplied heading into the warmer months.

Looking Ahead

With the next report scheduled for May 7, market participants will be watching closely to see whether injections maintain this pace. Sustained builds above historical norms could further widen the storage surplus, while any slowdown may tighten expectations heading into peak summer demand.

Overall, this report reinforces a familiar seasonal narrative: inventories are rebuilding efficiently, supply is ample, and the market is entering a period where weather will increasingly dictate direction.

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Source: https://ir.eia.gov/ngs/ngs.html

Start futures forex fx commodity news trading with Haawks G4A low latency machine-readable data, one of the fastest data feeds for DOE data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.