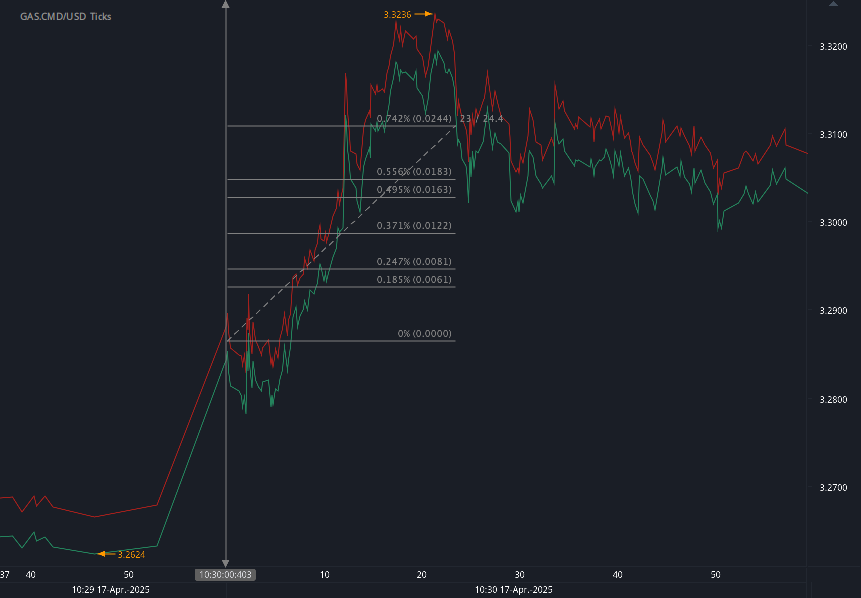

According to our analysis USDJPY moved 9 pips and US500 moved 3 points on US Jobless Claims data on 8 May 2025.

USDJPY (9 pips)

US500 (3 points)

Charts are exported from JForex (Dukascopy).

U.S. Weekly Jobless Claims Drop as Labor Market Remains Resilient

Published: May 8, 2025

The U.S. labor market showed signs of stability this week as initial unemployment insurance (UI) claims decreased, according to the latest data released by the Department of Labor. For the week ending May 3, seasonally adjusted initial claims for unemployment benefits fell to 228,000, down by 13,000 from the previous week’s unrevised figure of 241,000.

Key Takeaways:

Initial claims (seasonally adjusted): 228,000 (↓13,000 from prior week)

4-week moving average: 227,000 (↑1,000 from previous week)

Insured unemployment rate (seasonally adjusted): 1.2% (↓0.1%)

Insured unemployment level: 1,879,000 (↓29,000 from the prior week)

Despite a small uptick in the four-week moving average for initial claims, the overall decline in weekly claims suggests that layoffs remain relatively contained.

Unadjusted Numbers Highlight Broader Declines

Unadjusted data showed an even more pronounced drop. The number of actual initial claims under state programs fell to 206,937, a decline of 16,972 claims, or 7.6%, from the previous week. This was notably more than the expected seasonal decrease of just 4,584 claims.

When compared to the same period last year, initial claims are slightly below the 210,050 reported in early May 2024, indicating that the labor market remains historically tight.

Continued Claims Edge Lower

Continued claims, which reflect the number of people receiving ongoing benefits, also saw a decrease. For the week ending April 26:

Seasonally adjusted insured unemployment fell to 1,879,000 (↓29,000).

The four-week moving average rose slightly to 1,874,500.

The unadjusted insured unemployment rate held steady at 1.2%.

State-Level Insights

Some states saw significant changes in initial claims:

Increases:

New York: +15,418 (layoffs in transportation, accommodation, food services, education, and public administration)

Massachusetts: +3,301 (education sector)

Georgia: +1,207

Puerto Rico: +1,012

Decreases:

Connecticut: -2,340

Rhode Island: -1,850

Missouri: -1,696

Michigan: -1,436

The largest insured unemployment rates were seen in New Jersey and Rhode Island (2.5%), followed by California (2.3%) and Washington (2.1%).

Federal Program Activity

Federal unemployment programs remained largely unchanged. Claims filed by former federal civilian employees totaled 468, while newly discharged veterans filed 339 initial claims. Continued weeks claimed by both groups showed minimal movement.

Conclusion

This week’s decline in initial and continued claims underscores the resilience of the U.S. labor market, even amid sector-specific layoffs. While certain states and industries are experiencing localized job losses, overall jobless claim levels remain consistent with a healthy employment environment.

As economic uncertainties persist, analysts will be watching these weekly claims numbers closely for early signs of a broader labor market shift.

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Sources: https://www.dol.gov/ui/data.pdf

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.

Start futures forex fx news trading with Haawks G4A low latency machine-readable data today, one of the fastest news data feeds for US macro-economic and commodity data.